New Blog Article Facebook Post – 2026-01-21T155418.301")

Managing tax compliance in Malaysia goes beyond payroll and PCB deductions.

For business owners, freelancers, landlords, and self-employed individuals, CP500 is a key obligation that cannot be ignored.

Each year, the Inland Revenue Board of Malaysia (LHDN) issues CP500 tax instalment notices to individuals with non-salary income, requiring them to pay income tax in advance—long before the annual tax return is filed.

This employer-focused guide explains what CP500 is, who must pay it, payment deadlines, revision rules, and how to stay compliant without disrupting cash flow.

What Is CP500 in Malaysia?

CP500 (Notis Bayaran Ansuran) is an income tax instalment scheme introduced by LHDN for individuals who earn non-employment income, such as:

-

Business or professional income

-

Freelance or self-employment income

-

Rental income

-

Royalties or commissions

Unlike salaried employees—whose taxes are deducted monthly via PCB (Potongan Cukai Bulanan)—these individuals must pay estimated tax in advance through CP500.

Instead of settling a large tax bill at year-end, CP500 spreads the payment across six bi-monthly instalments, helping taxpayers manage cash flow while ensuring timely tax collection.

Who Is Required to Pay CP500?

CP500 applies strictly to individual taxpayers with non-salary income, including:

-

Sole proprietors and partners

-

Freelancers and consultants

-

Landlords earning rental income

-

Individuals receiving royalties

-

Self-employed professionals

❌ Who Does NOT Need CP500?

-

Employees earning fixed salary only

-

Individuals whose taxes are fully covered by PCB

Important: Not receiving a CP500 notice does not automatically mean you are exempt. If you earn taxable non-salary income, you are still legally required to declare and pay tax.

Who Will Receive Form CP500 from LHDN?

LHDN typically issues CP500 notices in February to individuals who:

-

Declared non-salary income in the previous year, or

-

Have an existing business or rental tax profile

The CP500 notice includes:

-

Estimated tax payable for the year

-

Instalment amounts

-

Six scheduled due dates

If your business has ceased operations or income has significantly dropped, you must actively apply for a revision—CP500 is not cancelled automatically.

CP500 Payment Schedule & Due Dates

The CP500 installment payments are due every two months according to the schedule set by LHDN. The payment dates are:

-

30 March

-

30 May

-

30 July

-

30 September

-

30 November

-

30 January (following year)

Each payment must be made within 30 days of the due date. Late payment triggers a 10% penalty on the outstanding amount—automatically imposed by LHDN.

Didn’t Receive CP500? What Employers Should Do

If a taxpayer does not receive CP500 by the end of February, they should:

-

Log in to MyTax to check if the CP500 notice is available online.

-

Call the Hasil Care Line for assistance.

-

Visit the nearest LHDN branch

Not receiving CP500 does not mean a taxpayer is exempt from paying tax. If business income is earned, tax may still be due at the end of the year.

Can I Revise CP500 Installment? (Form CP502 Explained)

Yes. Taxpayers may apply to revise CP500 instalments if:

-

Business income has dropped

-

Operations have ceased

-

Cash flow has changed significantly

To revise CP500, taxpayers must:

- Submit Form CP502 to LHDN before 30 June of the current assessment year.

-

Provide evidence of lower income, such as business records or financial statements.

-

Wait for LHDN to review and confirm the new CP500 installment amount.

However, if the revised amount is more than 30% lower than the actual tax payable, LHDN may impose a 10% penalty for underpayment.

If a business has closed down or is no longer profitable, taxpayers should submit Form CP502 as early as possible to stop CP500 deductions.

How to Calculate CP500 Tax Installments

The CP500 amount is calculated based on your previous year’s tax assessment, with LHDN estimating your tax liability and splitting it into six bi-monthly installment payments.1. Estimate Your Annual Taxable Income

Include all non-salary earnings:- Business profits

- Rental income

- Freelance/commission earnings

- Other taxable income

2. Determine Taxable Amount After Deductions

Deduct allowable expenses and reliefs such as:- EPF (Employee Provident Fund) contributions

- SOCSO/Perkeso

- Insurance premiums

- Education, medical, and lifestyle reliefs

3. Apply the Progressive Tax Rates

Malaysia uses a progressive tax rate system ranging from 0% to 30% depending on income brackets. Example (for YA 2024):- RM0 – RM5,000: 0%

- RM5,001 – RM20,000: 1%

- RM20,001 – RM35,000: 3%

- RM35,001 – RM50,000: 8%

- RM50,001 – RM70,000: 13%

- RM70,001 – RM100,000: 21%

- RM100,001 – RM250,000: 24%

- RM250,001 – RM400,000: 25%

- RM400,001 – RM600,000: 26%

- RM600,001 – RM2,000,000: 28%

- RM2,000,001 and above: 30%

4. Compute the Estimated Tax Payable

Use the tax brackets above to calculate the total tax due. Example: If your taxable income is RM80,000:- First RM35,000 = RM400 tax

- Next RM15,000 = RM1,200 tax

- Next RM15,000 = RM1,950 tax

- Next RM15,000 = RM3,150 tax

- Total Tax Payable: RM6,700

5. Divide into CP500 Installments

LHDN typically divides your estimated tax into six payments across the year. Using the RM6,700 example: RM6,700 ÷ 6 = RM1,116.67 per installmentHow LHDN Determines the CP500 Amount

LHDN calculates the estimated tax payable based on:

-

The taxpayer’s reported non-salary income from the previous year.

-

The applicable tax rate based on Malaysia’s tax structure.

-

The assumption that the taxpayer will earn a similar amount in the current year.

Because this amount is an estimate, business owners whose income changes significantly can request a revision of CP500 by submitting Form CP502 before 30 June.

How Employers Should Prepare for CP500 Payments

For sole proprietors and business owners, CP500 instalments should be included in regular financial planning. As the payments are based on past income, early preparation helps prevent cash flow issues and penalties.

Businesses should:

-

Review the CP500 notice once issued (usually in February) to confirm instalment amounts and due dates.

-

Plan cash flow for bi-monthly payments without affecting day-to-day business expenses.

-

Set aside funds monthly to avoid missed payments or late penalties.

-

Apply for a CP500 revision early if current income is lower than the previous year.

How to Pay CP500

CP500 payments can be made via:

-

MyTax Portal (online)

-

FPX internet banking

-

Bank counters

-

POS Malaysia counters (Cheque or cash deposits)

-

LHDN payment centers

Always verify your CP500 bill number before payment to avoid misallocation.

Penalties for Late or Non-Payment of CP500

Non-compliance carries serious consequences:

-

10% penalty for late instalments

-

Additional enforcement actions by LHDN

-

Higher year-end tax payable

-

Business cash-flow disruption

If a taxpayer cannot pay on time, they may request an installment plan from LHDN, but late penalties still apply.

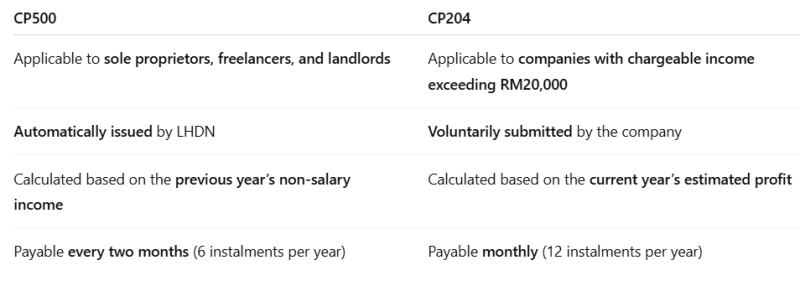

CP500 vs CP204: What’s the Difference?

Many employers operate both a company (CP204) and a sole proprietorship (CP500)—each must be managed separately.

Conclusion: CP500 Is Not Optional—Plan Early

CP500 is a mandatory tax instalment, not a suggestion.

For employers, freelancers, and business owners, ignoring it leads to penalties, cash-flow stress, and compliance risks.

By understanding CP500 early, reviewing instalments accurately, and planning payments strategically, businesses can meet tax obligations without operational disruption.