New Blog Article Facebook Post – 2026-03-09T174620.448")

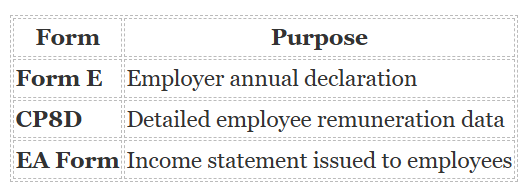

For employers in Malaysia, annual payroll tax reporting is an important compliance responsibility. Alongside Form E and EA Form, another key document that companies must prepare is CP8D.

Many employers are familiar with issuing EA Forms to employees, but may not fully understand the purpose of CP8D submission to LHDN.

In simple terms, CP8D provides detailed employee remuneration data to the Inland Revenue Board of Malaysia (LHDN). It allows the tax authority to verify salary information, cross-check monthly tax deductions (PCB), and ensure accurate income reporting.

As Malaysia continues strengthening digital tax enforcement through the MyTax system and e-Data Praisi, CP8D has become an essential part of employer compliance.

This guide explains what CP8D is, why it matters, who must submit it, deadlines, and how employers can prepare it correctly.

What Is CP8D?

CP8D is an annual employer return that contains detailed information about remuneration paid to employees during a specific tax year.

It is submitted to LHDN together with Form E and provides a breakdown of payroll data for each employee.

The information typically includes:

-

Employee identification details

-

Total annual remuneration

-

Salary, bonuses, and allowances

-

Benefits-in-kind (BIK) and perquisites

-

Director’s fees (if applicable)

-

PCB (Monthly Tax Deduction) totals

-

EPF contributions

While Form E summarises the company’s total remuneration, CP8D provides detailed employee-by-employee data.

To understand it simply:

Together, these forms ensure that employee income reporting remains accurate and transparent.

Why CP8D Is Important

Malaysia’s income tax system relies heavily on Monthly Tax Deduction (PCB), which acts as an advance payment of employees’ income tax.

CP8D helps LHDN verify whether the tax deductions made by employers are accurate.

With CP8D data, LHDN can:

-

Cross-check PCB deductions against total remuneration

-

Verify employee income declared in e-Filing

-

Identify payroll discrepancies

-

Detect under-reporting of income

-

Match employer payroll records with EA Forms

Without CP8D, LHDN would rely only on summary declarations and employee reporting.

CP8D therefore strengthens transparency in payroll reporting and tax compliance.

Legal Basis for CP8D

The requirement for CP8D comes from Rule 8D of the Income Tax (Deduction from Remuneration) Rules 1994.

Under Rule 8D, employers are required to:

-

Prepare an annual return of remuneration paid to employees

-

Submit the report in the format prescribed by LHDN

-

Ensure PCB deductions are correctly reported

-

Submit the return before the official deadline

Failure to comply with Rule 8D may lead to penalties under the Income Tax Act 1967.

This means CP8D is not optional — it is a statutory reporting requirement for employers in Malaysia.

Who Must Submit CP8D?

All employers who paid remuneration to at least one employee during the year of assessment must submit CP8D.

This includes:

-

Private limited companies (Sdn Bhd)

-

Public listed companies (Berhad)

-

SMEs and startups

-

Sole proprietorships with employees

-

Partnerships with staff

-

Representative offices

-

Foreign companies employing Malaysian workers

-

Companies with only one employee

Even if a company is small or newly established, CP8D submission is still required if remuneration was paid.

When Is CP8D Not Required?

If a company did not employ any staff during the year, CP8D submission is not required.

However, the employer must still submit Form E declaring “Nil Remuneration.”

Important points:

-

Form E submission is still mandatory

-

CP8D employee data file is not required

-

Failure to submit Form E may still result in penalties

This ensures that LHDN has confirmation that no payroll activity occurred during the year.

What Information Must Be Included in CP8D?

CP8D contains detailed payroll data for each employee.

Typical information includes:

Employee Details

-

Full name

-

NRIC or passport number

-

Income tax reference number

Income Information

-

Gross annual salary

-

Bonuses

-

Allowances

-

Commission or incentives

Additional Benefits

-

Benefits-in-kind (BIK)

-

Perquisites

-

Director’s fees (if applicable)

Tax & Statutory Contributions

-

PCB deductions

-

EPF contributions

Accuracy is critical because LHDN systems automatically compare this data with employee tax declarations.

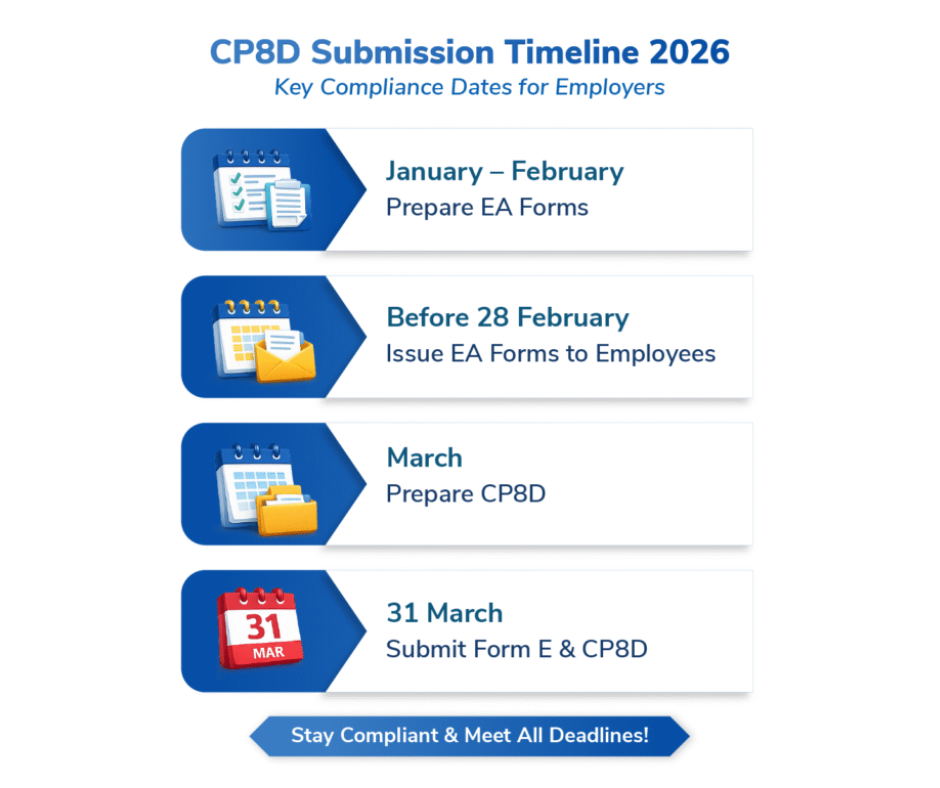

CP8D Submission Timeline for Employers

Employers must follow the annual tax reporting schedule.

January – February

Prepare EA Forms for employees.

Before 28 February

Issue EA Forms to employees for personal tax filing.

March

Prepare Form E and CP8D data.

31 March

Submit Form E together with CP8D to LHDN.

Submitting early helps employers avoid last-minute errors or technical issues.

How to Submit CP8D

Most employers now submit CP8D electronically through the MyTax portal.

The process typically involves three steps.

Step 1: Reconcile Year-End Payroll

Before preparing CP8D, employers should reconcile their payroll records with:

-

Annual payroll reports

-

Monthly PCB submissions (CP39)

-

EPF contributions

-

EA Forms issued to employees

This ensures all data matches.

Step 2: Generate the CP8D File

Employers can generate the CP8D file by:

-

Using LHDN’s e-Data Praisi software

-

Exporting data from payroll software

-

Formatting the file according to LHDN’s required structure

Incorrect formatting may cause submission errors.

Step 3: Submit Through MyTax

Employers then:

-

Log in to the MyTax employer account

-

Complete Form E

-

Upload the CP8D file

-

Validate and submit

-

Download the submission acknowledgment receipt

Employers should keep this receipt for audit purposes.

CP8D Submission Deadline

The key deadlines employers must remember are:

Late submission may result in:

-

Fines ranging from RM200 to RM20,000

-

Possible legal action

-

Higher audit risk

-

Compliance flags in LHDN’s system

Submitting on time helps businesses avoid these issues.

Common CP8D Mistakes Employers Should Avoid

Some common compliance errors include:

-

Mismatched payroll data and EA Forms

-

Incorrect PCB reporting

-

Missing employee records

-

Late submission

-

Formatting errors in CP8D files

Proper payroll reconciliation helps reduce these risks.

How Payroll Systems Help With CP8D Compliance

Preparing CP8D manually can be challenging, especially for companies with many employees.

Using a digital payroll system helps employers:

-

Maintain accurate payroll records

-

Track PCB deductions automatically

-

Generate CP8D-ready reports

-

Reduce manual errors

-

Stay compliant with Malaysian tax regulations

With Pandahrms, employers can streamline payroll processing and maintain organised records that support annual tax reporting and compliance requirements.

Conclusion

CP8D is an essential part of Malaysia’s employer tax compliance framework.

It provides LHDN with detailed employee remuneration data, ensuring that payroll information, PCB deductions, and employee tax filings remain consistent.

For employers, preparing CP8D correctly is more than a filing requirement. It is also an opportunity to:

-

Verify payroll accuracy

-

Reduce compliance risks

-

Maintain proper documentation

-

Avoid penalties and audit issues

By understanding CP8D obligations and preparing early, employers can ensure smooth annual tax reporting and stronger payroll compliance.