New Blog Article Facebook Post (22)")

PERKESO LINDUNG 24 Jam Is Now Optional—Should You Keep It?

Since the Malaysian Government announced that PERKESO LINDUNG 24 Jam is no longer mandatory for Malaysian employees, one question has dominated social media, HR groups, and workplace discussions:

“I already have Personal Accident (PA) Insurance. Should I opt out of LINDUNG 24 Jam?”

It’s a reasonable question.

After all, both LINDUNG 24 Jam and Personal Accident (PA) Insurance provide protection against accidents. At first glance, they may seem to offer the same benefits.

But they are not the same product.

In fact, they serve different purposes, provide different types of benefits, and are designed to protect employees in different ways.

Choosing whether to keep or opt out of LINDUNG 24 Jam shouldn’t be based solely on the monthly contribution. Instead, employees should understand what each scheme covers, where they overlap, and what protection they may lose by opting out.

In this guide, we’ll explain everything employers, HR professionals, and employees need to know.

Latest Policy Update (8 July 2026)

Before comparing the two, here’s a quick recap of the latest policy changes.

As announced by the Malaysian Government:

Malaysian Employees

- Participation is now voluntary (opt-out basis).

- Employees who do nothing will continue participating in the scheme.

- Employees may choose to opt out following PERKESO’s official process.

Foreign Employees

Nothing has changed.

LINDUNG 24 Jam remains mandatory under existing legal provisions.

Since the implementation mechanism may continue to evolve, employers and employees should always refer to the latest announcements from PERKESO and the Ministry of Human Resources (KESUMA).

What Is PERKESO LINDUNG 24 Jam?

PERKESO LINDUNG 24 Jam, officially known as the Skim Kemalangan Bukan Bencana Kerja, is Malaysia’s social security scheme that protects employees against eligible accidents occurring outside working hours.

Previously, PERKESO mainly covered:

- Workplace accidents

- Occupational injuries

- Certain commuting accidents

However, many accidents happen during employees’ personal time.

For example:

- Slipping in the bathroom

- Falling from a ladder while repairing your house

- Weekend football injuries

- Motorcycle accidents during personal travel

- Cycling accidents

- Recreational injuries

LINDUNG 24 Jam was introduced to fill this protection gap.

Instead of protecting employees only while working, it extends coverage to eligible non-work-related accidents occurring within Malaysia.

What Is Personal Accident (PA) Insurance?

Personal Accident (PA) Insurance is a private insurance product offered by insurance companies or takaful operators.

Unlike PERKESO, PA is a commercial insurance plan.

Coverage depends entirely on the policy purchased.

A typical PA plan may include:

- Accidental death benefit

- Permanent disability benefit

- Accident medical reimbursement

- Hospital income allowance

- Ambulance fees

- Fracture benefits

- Additional optional riders

However, every insurance company offers different benefits.

Some plans include worldwide protection.

Others only cover accidents within Malaysia.

Some include extreme sports.

Others exclude them.

This is why employees should never compare insurance products based only on their names.

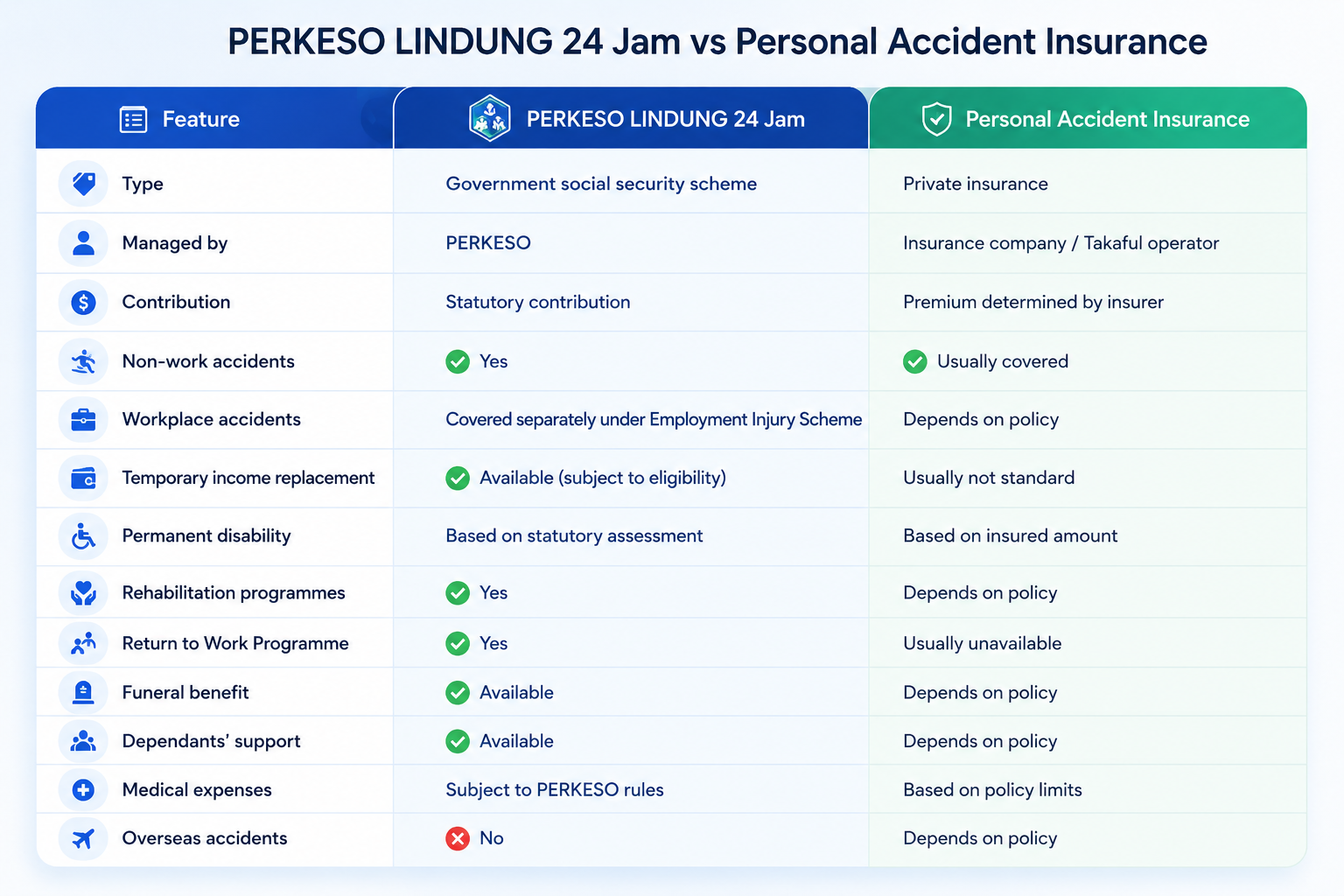

LINDUNG 24 Jam vs Personal Accident Insurance

Although both provide accident protection, they work very differently.

The biggest takeaway?

LINDUNG 24 Jam focuses on long-term social protection.

PA Insurance focuses on financial compensation based on the insurance coverage purchased.

Neither automatically replaces the other.

What Does LINDUNG 24 Jam Offer That Many PA Policies Don’t?

Many employees compare only one number:

“How much will my family receive if I die?”

But LINDUNG 24 Jam is much more than a death benefit.

Let’s look at what makes it different.

1. Temporary Income Replacement

Imagine this scenario.

You fracture your leg during a weekend hiking trip.

Your doctor certifies two months of medical leave.

During this period, you cannot work.

LINDUNG 24 Jam may provide a Temporary Disablement Benefit, subject to PERKESO’s eligibility requirements.

Many basic PA insurance plans don’t provide monthly income replacement simply because you’re temporarily unable to work.

2. Long-Term Disability Support

If an accident causes permanent disability, LINDUNG 24 Jam doesn’t simply issue a one-time payment.

Benefits are assessed based on:

- Medical assessment

- Degree of disability

- Employee wages

- Age

- PERKESO regulations

Some benefits may be paid periodically rather than as a single lump sum.

The objective is long-term financial support.

Private PA Insurance usually works differently.

The insurer pays according to the policy’s disability percentage table and insured amount.

3. Rehabilitation Services

This is one of LINDUNG 24 Jam’s strongest advantages.

Recovery isn’t only about hospital bills.

Employees may require:

- Physiotherapy

- Occupational therapy

- Artificial limbs

- Wheelchairs

- Rehabilitation equipment

- Return to Work programmes

These services help injured employees regain independence and return to employment.

Most PA insurance policies focus mainly on financial payouts rather than rehabilitation.

Where Personal Accident Insurance May Provide Better Protection

That doesn’t mean PA Insurance is inferior.

In many situations, it offers benefits LINDUNG 24 Jam cannot provide.

Higher Lump Sum Coverage

Employees can choose their own insured amount.

For example:

- RM100,000

- RM300,000

- RM500,000

- RM1 million

The larger the insured amount, the larger the potential payout.

PERKESO benefits, however, follow statutory formulas instead of fixed insured amounts.

Overseas Protection

LINDUNG 24 Jam generally protects accidents occurring within Malaysia.

Employees who frequently travel overseas may benefit from PA Insurance offering worldwide coverage.

Flexible Add-On Benefits

Many insurers offer optional benefits including:

- Daily hospital income

- Fracture allowance

- Ambulance fees

- Emergency medical evacuation

- Family support benefits

Coverage varies depending on the insurance policy.

Three Common Misconceptions

Myth 1: “I Already Have a Medical Card.”

A medical card mainly pays hospital expenses.

It usually doesn’t replace your salary while you’re recovering.

Neither does it necessarily provide disability income or rehabilitation support.

Myth 2: “I Already Bought PA Insurance.”

Not every PA policy includes:

- Temporary disability income

- Rehabilitation

- Long-term wage replacement

Always read the policy schedule carefully.

Myth 3: “The Contribution Is Small, So I Should Definitely Keep It.”

Or the opposite.

“It’s another salary deduction, so I’ll definitely opt out.”

Both viewpoints may oversimplify the decision.

Instead, ask yourself:

- Do I have enough insurance?

- Can my family survive if I cannot work for several months?

- What happens if I become permanently disabled?

- How much emergency savings do I have?

The decision should depend on your financial situation—not just the monthly deduction.

Who Should Consider Keeping LINDUNG 24 Jam?

You may want to remain enrolled if:

- You don’t own Personal Accident Insurance.

- Your family depends heavily on your salary.

- You frequently ride motorcycles.

- You regularly participate in sports or outdoor activities.

- You have limited emergency savings.

- You value PERKESO’s rehabilitation services.

- Your employer doesn’t provide extensive insurance benefits.

- You’re older and private insurance premiums have become expensive.

Who May Consider Opting Out?

Some employees may already have comprehensive protection.

For example:

- High-value Personal Accident Insurance.

- Employer-provided accident coverage.

- Disability income protection.

- Comprehensive medical insurance.

- Adequate emergency savings.

Even then, employees should compare benefits carefully before deciding.

Remember:

Opting out means giving up the protection provided by LINDUNG 24 Jam.

Make sure your existing insurance genuinely covers the same risks—not just similar-sounding benefits.

A Simple Example

Let’s compare two situations.

Amin

- Monthly salary: RM4,000

- Personal Accident Insurance:

- RM200,000 accidental death

- RM200,000 permanent disability

- RM5,000 medical expenses

One weekend, Amin slips while washing his car and fractures his leg.

He cannot work for two months.

His PA insurance may reimburse eligible medical expenses.

However, unless his policy specifically includes temporary disability income, it may not replace his lost earnings during recovery.

If Amin remains covered under LINDUNG 24 Jam and meets PERKESO’s eligibility requirements, he may qualify for temporary disablement benefits in addition to medical support.

Now imagine the accident causes permanent disability.

PA Insurance may provide a lump-sum payout according to the insured amount.

LINDUNG 24 Jam may provide ongoing disability benefits, rehabilitation support, and Return to Work assistance.

This illustrates why many financial planners view the two as complementary rather than competing forms of protection.

What HR and Employers Should Know

Although the latest policy affects employees, HR and Payroll departments also have important responsibilities.

Organisations should:

- Stay updated with PERKESO announcements.

- Understand the official opt-out process.

- Update payroll deductions where required.

- Keep accurate employee contribution records.

- Communicate policy changes clearly to employees.

Providing employees with accurate information helps reduce confusion and supports better financial decision-making.

How Pandahrms Helps Employers Manage Statutory Changes

Employment regulations change frequently.

With Pandahrms, employers can streamline HR and payroll operations through:

- Payroll automation

- Statutory contribution management

- Employee database management

- Attendance tracking

- Leave management

- Compliance reporting

- HR dashboards

- Secure employee records

As statutory requirements continue to evolve, an integrated HR and Payroll system helps businesses remain compliant while reducing manual administrative work.

Conclusion

The question isn’t whether LINDUNG 24 Jam is better than Personal Accident Insurance.

The better question is:

Do you fully understand what each one protects?

LINDUNG 24 Jam is designed as a social security scheme that provides more than accident compensation. It includes income replacement, rehabilitation, disability support, and long-term assistance for eligible employees.

Personal Accident Insurance, on the other hand, offers flexible protection with customisable insured amounts and optional benefits depending on the policy you purchase.

For many Malaysians, the two can work together rather than replace one another.

Before deciding whether to opt out, take the time to review your insurance coverage, financial responsibilities, and family needs. A small monthly saving today may not outweigh the protection you could need after a serious accident.

Frequently Asked Questions (FAQ)

1. Is LINDUNG 24 Jam the same as Personal Accident Insurance?

No. LINDUNG 24 Jam is a PERKESO social security scheme, while Personal Accident Insurance is a private insurance product. They differ in benefit structure, coverage, and claim assessment.

2. Can I claim both LINDUNG 24 Jam and Personal Accident Insurance?

Generally, yes. Having private insurance does not automatically prevent you from claiming eligible benefits under LINDUNG 24 Jam. However, claims are subject to PERKESO’s rules and your insurance policy terms.

3. Should I opt out if I already have Personal Accident Insurance?

Not necessarily. Compare your existing coverage carefully. Some PA policies may not provide income replacement, rehabilitation, or long-term disability support similar to LINDUNG 24 Jam.

4. Is LINDUNG 24 Jam still mandatory?

For Malaysian employees, participation is now voluntary under the latest government policy. Foreign workers remain subject to mandatory participation under existing legal provisions.

5. Does LINDUNG 24 Jam cover accidents outside Malaysia?

Generally, no. The scheme primarily covers eligible non-work-related accidents occurring within Malaysia, subject to PERKESO’s terms and conditions.