New Blog Article Facebook Post – 2026-02-07T130849.059")

LHDN Stamp Duty PKPS 2026: 100% Penalty Waiver for Late Stamping

Employer & Business Compliance Guide (Malaysia)

If your business has agreements or legal documents signed between 1 January 2023 and 31 December 2025 that were never stamped—or were stamped late—this is a rare compliance window you should not ignore.

The Inland Revenue Board of Malaysia (LHDN) has officially introduced the Stamp Duty Special Voluntary Disclosure Programme (PKPS) 2026, offering a full waiver (100%) of late stamping penalties, subject to strict timelines and conditions.

This article explains what PKPS 2026 is, who qualifies, key deadlines, and what employers and businesses should do now to reduce compliance risk.

What Is the Stamp Duty PKPS 2026?

The Stamp Duty Special Voluntary Disclosure Programme (PKPS) 2026 is a limited-time compliance initiative by LHDN that allows taxpayers to regularise late or unpaid stamp duty without incurring penalties under the Stamp Act 1949.

Under PKPS 2026:

-

Eligible documents may be stamped after the execution date

-

100% of late stamping penalties are waived

-

No appeal or manual penalty remission request is required

-

Penalty waiver is applied automatically at payment stage

This programme is time-bound and will not be extended automatically.

Who Is Eligible for PKPS Stamp Duty 2026?

Eligibility is determined by document date and payment status, not by taxpayer size or industry.

Eligible Documents

Documents that meet all of the following conditions qualify:

-

Executed between 1 January 2023 and 31 December 2025

-

Either:

-

Not stamped at all, or

-

Stamped but stamp duty not yet paid

-

📌 Documents already submitted for assessment before 2026, but with unpaid duty, remain eligible.

Eligible Taxpayers

-

Individuals

-

Businesses and employers

-

Malaysian and non-Malaysian taxpayers

What Benefits Does PKPS 2026 Provide?

The programme offers full penalty remission, not partial relief.

Key Benefits

✅ 100% waiver of late stamping penalties

✅ No appeal or justification required

✅ Automatic waiver upon payment

✅ Documents stamped under PKPS will not be audited

⚠️ Important compliance note

Your Notice of Assessment or BNDS may still display a penalty amount. This is system-generated. The penalty will be automatically removed during payment within the PKPS period.

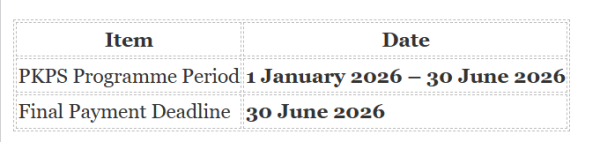

PKPS Stamp Duty 2026: Key Dates Employers Must Track

Missing the deadline means losing the waiver entirely.

❌ Any payment made after 30 June 2026 will be subject to normal late penalties under the Stamp Act.

How to Participate in PKPS Stamp Duty 2026

There is no separate application for PKPS.

Step-by-Step Process

-

Submit eligible documents via e-Duti Setem

-

Receive assessment / BNDS

-

Make payment within the PKPS period

-

Penalty waiver is applied automatically

📌 Manual submissions are not allowed. All stamping must be completed online.

Important Conditions and Exclusions

Before proceeding, employers should note the following limitations.

Not Eligible Under PKPS

❌ Documents involving fraud, falsification, or intentional evasion

❌ Documents executed in 2026

Additional Compliance Points

-

Documents stamped under PKPS will not be audited

-

LHDN may still audit other documents outside the programme

-

Documents fully stamped and paid (including penalties) before 1 January 2026 are not eligible for refunds

Why PKPS 2026 Matters for Employers and Businesses

Many organisations underestimate stamp duty exposure until an audit occurs.

Common high-risk documents include:

-

Employment contracts

-

Tenancy and rental agreements

-

Loan and financing documents

-

Share transfer instruments

-

Commercial agreements and addendums

Penalties for late stamping can be substantial, especially when multiple documents are involved.

PKPS 2026 provides a risk-free opportunity to:

-

Rectify historical non-compliance

-

Reduce audit exposure

-

Avoid unnecessary penalty costs

Frequently Asked Questions (FAQ) – PKPS Stamp Duty 2026

(Updated: 28 January 2026)

1. When does PKPS Stamp Duty 2026 start and end?

PKPS runs from 1 January 2026 to 30 June 2026. Both stamping and payment must be completed within this period.

2. What documents qualify under PKPS 2026?

All instruments executed between 1 January 2023 and 31 December 2025 that remain unstamped or unpaid.

3. Can applications be submitted manually?

No. All submissions must be completed via e-Duti Setem.

4. If stamping was done earlier but payment was not made, is it still eligible?

Yes. Penalty exemption applies as long as payment is made within the PKPS period.

5. Is an appeal required to obtain the penalty waiver?

No. The waiver is automatic upon payment.

6. Why does the BNDS still show a penalty?

The system may display penalties initially, but they are removed automatically at payment stage.

7. Are documents already fully paid before 2026 eligible?

No. Fully settled cases before 1 January 2026 are excluded.

8. Will documents stamped under PKPS be audited?

No. PKPS-stamped documents are excluded from stamp duty audit.

9. Are fraud cases eligible?

No. Any form of fraud or intentional evasion is excluded.

10. Does PKPS apply to non-Malaysians?

Yes. The programme applies to all taxpayers.

11. What happens if payment is made after 30 June 2026?

Penalty exemption is withdrawn and late penalties will apply.

12. What if I ignore PKPS entirely?

Post-30 June 2026, unstamped documents may attract penalties and audit action under LHDN’s Stamp Duty Audit Framework.

Final Compliance Reminder for Employers

PKPS Stamp Duty 2026 is a one-time compliance relief, not a recurring amnesty. Employers should review historical agreements early to avoid last-minute processing delays before 30 June 2026.

From a governance perspective, tracking document execution dates, stamping status, and compliance deadlines is critical. Many employers now centralise employment contracts, agreements, and compliance records digitally to reduce oversight risk—especially during audits or statutory reviews.

A structured HR and document management system helps ensure agreements are properly recorded, tracked, and aligned with statutory obligations, supporting stronger long-term compliance beyond PKPS 2026.