New Blog Article Facebook Post – 2026-04-07T180450.805")

Introduction: PCB — A Critical Part of Payroll Compliance

Every month, employers in Malaysia deduct a portion of employees’ salaries for income tax.

This system, known as Potongan Cukai Berjadual (PCB), ensures that employees pay their income tax progressively throughout the year instead of in a lump sum.

For employers, PCB is not optional. It is a statutory payroll obligation.

Incorrect PCB calculations or late submissions can result in:

- Compliance breaches

- Financial penalties

- Employee dissatisfaction

- Increased audit risk

This guide explains how PCB works, how it is calculated, and what employers must do to remain fully compliant in 2026.

What Is PCB (Potongan Cukai Bulanan)?

PCB refers to the monthly income tax deduction made by employers on behalf of employees.

The deducted amount is submitted to Lembaga Hasil Dalam Negeri (LHDN), Malaysia’s Inland Revenue Board.

Key Purpose of PCB:

- Spread tax payments across the year

- Reduce year-end tax burden for employees

- Improve tax collection efficiency

By the time employees file their annual tax return (Form BE), most or all of their tax liability has already been paid through PCB.

Why Is Tax Deducted Monthly From Salary?

PCB exists to prevent employees from facing a large tax payment at the end of the year.

Instead of paying a lump sum:

- Tax is deducted monthly

- Payments are based on estimated annual income

- Adjustments are made during annual tax filing

This approach benefits both employees and employers by ensuring consistent tax compliance and financial planning.

Who Is Required to Pay PCB?

1. Employees with Taxable Income

PCB applies to employees earning above the taxable income threshold set by LHDN.

As a general guideline:

- Individuals earning above approximately RM34,000 annually (after EPF deductions) are subject to income tax

2. Malaysian vs Non-Resident Employees

- Malaysian tax residents: Subject to progressive tax rates (0% to 30%)

- Non-residents: Subject to a flat tax rate of 30%

3. Self-Employed Individuals

Self-employed individuals and freelancers:

- Do not have PCB deductions

- Must manage and submit their own income tax directly to LHDN

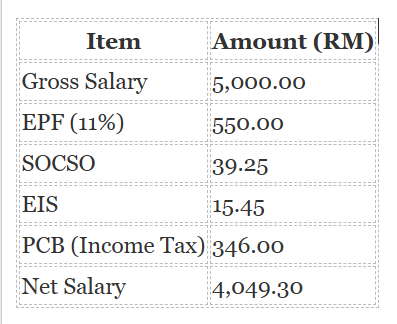

How PCB Appears on a Payslip

PCB is reflected as a deduction in an employee’s monthly payslip.

Example: Monthly Salary RM5,000

The PCB amount varies depending on:

- Salary level

- Reliefs and deductions

- Personal circumstances

How Employers Calculate PCB

PCB is not a simple division of annual tax by 12. It is calculated based on LHDN-prescribed formulas and schedules.

Key Factors in PCB Calculation:

1. Monthly Salary

Includes:

- Basic salary

- Fixed allowances

- Commissions and bonuses

2. Statutory Deductions

- EPF contributions

- SOCSO and EIS

These reduce taxable income.

3. Tax Reliefs

Certain reliefs may be considered if declared, such as:

- EPF contributions

- Insurance

- Personal reliefs (via TP1 form)

4. PCB Schedules / e-PCB System

Employers use:

- LHDN PCB tables

- e-PCB calculator

- Payroll software systems

to determine accurate monthly deductions.

Is PCB the Final Tax Payment?

No. PCB is an advance tax payment based on estimation.

At year-end, employees must file their income tax return (Form BE), where:

- Actual annual income is calculated

- All eligible tax reliefs are applied

- Final tax liability is determined

Possible Outcomes:

- Refund: If PCB paid exceeds actual tax

- Additional payment: If PCB is insufficient

Common Situations That Affect PCB Accuracy

1. Bonuses and Irregular Income

Additional income may:

- Increase total annual income

- Result in higher tax payable

2. Mid-Year Job Changes

New employers may:

- Not have full-year income data

- Underestimate PCB deductions

3. Unclaimed Tax Reliefs

If reliefs are not declared early:

- PCB may be higher than necessary

- Refunds occur during tax filing

4. Change in Personal Status

Marriage or children:

- Increase tax relief eligibility

- Affect final tax calculation

5. Multiple Income Sources

Additional income (freelance, rental):

- Not included in PCB

- Must be declared separately

Employer Responsibilities for PCB

Employers play a critical role in ensuring tax compliance.

1. Deduct PCB Monthly

- Calculate accurate PCB

- Deduct from employee salaries

- Reflect clearly in payslips

2. Submit PCB to LHDN

PCB must be submitted before the 15th of the following month.

Example:

- March payroll → Submit by 15 April

3. Register Employer Tax Account

Employers must register for an E Number via the MyTax portal.

4. Issue EA Form

At year-end, employers must provide employees with EA Form, which includes:

- Total annual income

- Total PCB deductions

How to Submit PCB Payments

Employers can submit PCB through:

- e-PCB system (monthly submission)

- e-Data PCB (bulk submission via payroll software)

- e-CP39 (manual submission)

- FPX online banking

Accurate and timely submission is essential to avoid penalties.

Penalties for Non-Compliance

Failure to comply with PCB requirements may result in:

- Fines up to RM20,000

- Imprisonment up to 6 months

- Additional penalties on unpaid tax

These penalties are enforced under the Income Tax Act 1967.

Practical HR and Payroll Actions

To ensure compliance, employers should:

1. Review Payroll Setup

- Ensure correct PCB formulas

- Align with LHDN requirements

2. Maintain Accurate Employee Records

- Salary structure

- Relief declarations (TP1 / TP3 forms)

3. Monitor Monthly Submissions

- Track submission deadlines

- Maintain payment records

4. Use Payroll Automation

- Reduce manual errors

- Ensure consistent compliance

Why Payroll Systems Are Essential for PCB Compliance

Manual payroll processing increases the risk of:

- Miscalculation of PCB

- Incorrect deductions

- Missed submission deadlines

A reliable payroll system ensures:

- Accurate tax calculations

- Automated statutory deductions

- Audit-ready reporting

How Pandahrms Supports PCB Compliance

Pandahrms helps employers:

- Automate PCB, EPF, SOCSO, and EIS calculations

- Ensure accurate payroll processing aligned with LHDN rules

- Manage employee tax data efficiently

- Generate statutory reports and EA Forms

- Maintain compliance across payroll operations

This is especially critical for businesses with:

- Large employee headcount

- Variable income structures (bonuses, commissions)

- Multi-entity payroll environments

FAQs: PCB in Malaysia

1. What is PCB in Malaysia?

PCB is a monthly income tax deduction made by employers on behalf of employees.

2. Is PCB mandatory?

Yes. Employers are legally required to deduct and submit PCB.

3. What is the PCB submission deadline?

Before the 15th of the following month.

4. Do employees still need to file taxes?

Yes. Annual tax filing is required to finalise tax liability.

5. What happens if PCB is incorrect?

Adjustments will be made during tax filing, resulting in refunds or additional payments.

6. Do freelancers pay PCB?

No. They are responsible for their own tax filings.

Conclusion: PCB Is More Than a Deduction — It Is a Compliance Obligation

PCB plays a critical role in Malaysia’s tax system by ensuring consistent and timely tax payments.

For employers, it is a core payroll responsibility that requires:

- Accurate calculation

- Timely submission

- Proper documentation

Failure to manage PCB correctly exposes businesses to legal, financial, and operational risks.

Simplify PCB and Payroll Compliance with Pandahrms

Managing PCB manually is complex and error-prone.

Pandahrms enables employers to:

- Automate statutory deductions

- Ensure payroll accuracy

- Maintain full compliance with LHDN regulations

- Reduce administrative workload

Schedule a personalised demo to see how Pandahrms can streamline your payroll and statutory compliance.