New Blog Article Facebook Post – 2026-04-20T170611.474")

Got a CP58 Form? Here’s What Malaysian Agents Need to Know Before Filing Taxes

You opened the envelope and saw a CP58 form.

Immediately, a few questions probably came to mind:

- What exactly is CP58?

- Do I need to pay tax?

- Should I file Form B or Form BE?

- Can I claim business expenses?

- Am I accidentally overpaying taxes?

Every year, many Malaysian insurance agents, property negotiators, MLM distributors, freelance dealers, and commission earners end up paying more tax than necessary simply because they misunderstand how CP58 income works.

Some file the wrong tax form.

Some forget to claim business expenses.

Others keep poor documentation and face problems during audits.

If you receive commission-based income in Malaysia, understanding CP58 properly is important — not only for tax filing, but also for compliance and income documentation.

This guide explains how CP58 works in Malaysia for YA 2025 / 2026 tax filing, including Form B, allowable deductions, personal reliefs, and common mistakes to avoid.

What Is a CP58 Form?

A CP58 is a statement of incentive payments issued under Section 83A of the Income Tax Act 1967.

Companies issue CP58 forms to agents, dealers, distributors, or other non-employees who receive:

- commissions

- bonuses

- incentives

- rewards

- non-cash benefits

If the total value exceeds RM5,000 in a calendar year, the company is generally required to issue a CP58 statement.

Importantly:

A CP58 is not a tax return.

It is a record of payments and incentives received from a company, which taxpayers use when filing income tax with LHDN.

Who Usually Receives CP58 Forms?

CP58 forms are commonly issued to:

- Insurance agents

- Property negotiators (REN)

- Unit trust consultants

- MLM distributors

- Direct sales agents

- Freelance commission earners

- Sales dealers

- Referral partners

Even if you work part-time, commission income may still require separate tax reporting.

What Income Appears on a CP58?

CP58 may include:

Cash Incentives

- commissions

- bonuses

- service incentives

- rebates

- referral fees

Non-Cash Rewards

- travel incentives

- vouchers

- gift cards

- electronics

- branded gifts

- overseas trips

Many taxpayers forget that non-cash rewards may still be taxable.

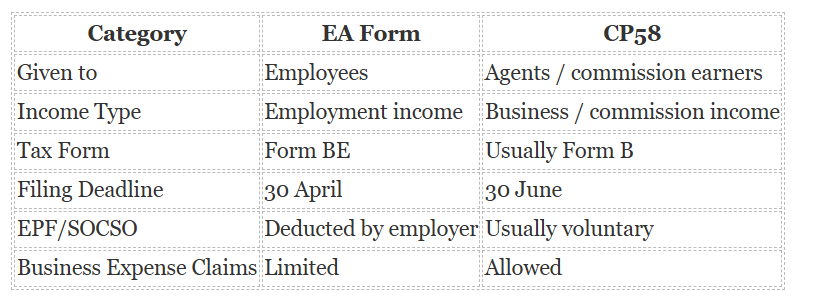

CP58 vs EA Form: What’s the Difference?

One of the biggest mistakes Malaysians make is confusing CP58 with EA Form income.

If you receive both:

- EA Form from employer

- CP58 from side income

You will generally file:

✅ Form B

Do CP58 Recipients Need to File Form B?

In most cases, yes.

Taxpayers earning commission or business-related income under CP58 will generally need to file Form B instead of Form BE.

This is important because:

Form B allows taxpayers to declare:

- business income

- commission income

- allowable business expenses

Filing incorrectly may cause taxpayers to:

- overpay taxes

- lose deduction opportunities

- face compliance issues later

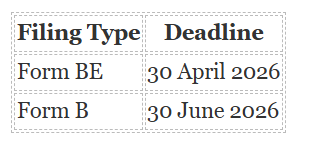

CP58 Filing Deadline Malaysia 2026

For income earned in 2025:

e-Filing extensions may apply depending on LHDN announcements.

Step-by-Step: What To Do After Receiving CP58

1. Check the Figures Carefully

Compare the CP58 totals against:

- commission statements

- payout reports

- bank records

Errors occasionally happen.

Request corrections early if needed.

2. Register for MyTax / e-Filing

You can register via:

3. Prepare Your Income Documentation

Organise:

- CP58 forms

- invoices

- receipts

- travel records

- marketing expenses

- bank statements

Good documentation is critical for audit support.

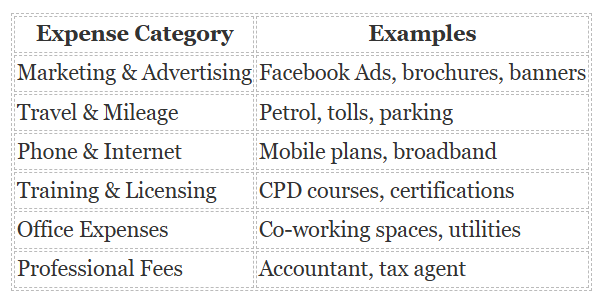

Business Expenses Many Agents Forget to Claim

This is where many commission earners unintentionally overpay taxes.

Because CP58 income is generally treated as business-related income, taxpayers may claim expenses incurred wholly and exclusively in generating income.

Common Allowable Business Expenses

Important Documentation Reminder

Always keep:

- receipts

- invoices

- payment records

- supporting documents

Taxpayers should retain records for at least:

✅ 7 years

Can You Claim Car Expenses?

Partially, yes.

Business-use vehicle expenses may qualify proportionally, including:

- petrol

- tolls

- parking

- maintenance

Vehicle claims may also involve capital allowance rules depending on the situation.

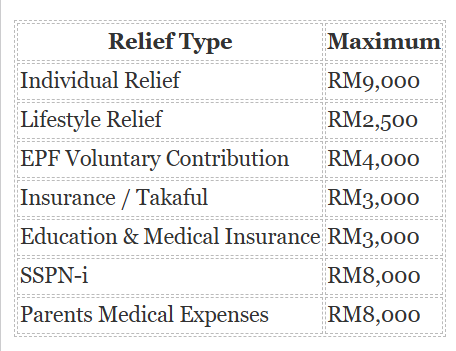

Personal Tax Reliefs You Can Still Claim

Receiving CP58 income does NOT remove eligibility for personal tax reliefs.

Common reliefs include:

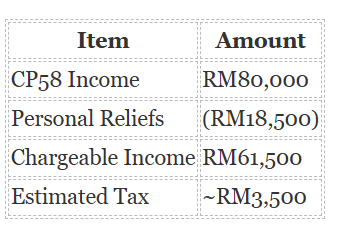

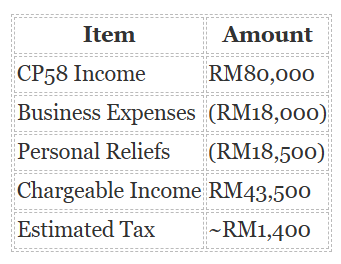

Example: How Proper Tax Planning Can Reduce Tax Payable

Scenario Without Expense Tracking

Scenario With Proper Expense Claims

Estimated tax savings:

✅ Approximately RM2,100

Illustrative example only. Actual tax payable depends on relief eligibility and tax computation.

Common CP58 Tax Filing Mistakes in Malaysia

Filing Form BE Instead of Form B

This is one of the most common mistakes.

Forgetting Business Expense Claims

Many taxpayers fail to claim:

- marketing

- travel

- phone

- licensing

- training expenses

Poor Record Keeping

Missing receipts may weaken audit defence.

Ignoring CP58 Because “No Tax Was Deducted”

Even if no tax was withheld:

- income may still be taxable

- LHDN still receives records from companies

What Happens If You Don’t Declare CP58 Income?

LHDN may:

- issue estimated tax assessments

- impose penalties

- deny unsubstantiated deductions

Additional penalties may apply for:

- late filing

- under-declaration

- non-compliance

Why Digital Income Documentation Matters More in 2026

Malaysia is moving toward:

- digital tax systems

- e-Invoice integration

- stronger audit trails

- automated compliance reporting

For commission earners and businesses alike, maintaining organised digital records is becoming increasingly important.

This includes:

- commission records

- reimbursement claims

- incentive tracking

- income documentation

Poor recordkeeping creates:

- audit risk

- tax disputes

- missing deductions

- payroll inconsistencies

How Digital Payroll & HR Systems Help Businesses Stay Organised

For businesses managing:

- agents

- incentive payments

- commissions

- allowances

- reimbursements

Digital HR and payroll systems help centralise:

- payment records

- documentation

- employee data

- statutory reporting

This improves:

✅ audit readiness

✅ payroll accuracy

✅ documentation tracking

✅ compliance management

FAQs About CP58 Malaysia

What if my CP58 income is below RM5,000?

You may still need to declare the income even if a CP58 was not issued.

What if the company never issued my CP58?

You are still responsible for declaring income received.

You may request the document from the company.

Can I claim business expenses without SSM registration?

Generally yes, depending on the nature of the income and supporting documentation.

Can I voluntarily contribute EPF as a self-employed agent?

Yes. Voluntary EPF contributions may also qualify for personal relief.

How long should I keep tax records?

At least:

✅ 7 years

Final Thoughts: Many Malaysians Overpay Tax Simply Because They File Incorrectly

CP58 income is often misunderstood.

Many agents:

- file the wrong form

- forget deductions

- keep poor records

- miss legitimate tax reliefs

Understanding how CP58 works can potentially save thousands of ringgit while reducing compliance risk.

As Malaysia moves toward greater digital tax compliance and e-Invoice integration, proper income documentation and organised records will become even more important.

Simplify Payroll, Documentation & Compliance with Pandahrms

Managing commissions, reimbursements, payroll records, and employee documentation manually can quickly become difficult as businesses grow.

Pandahrms helps businesses streamline:

- payroll management

- employee records

- claims tracking

- digital HR documentation

- compliance workflows

👉 Explore how Pandahrms helps Malaysian businesses simplify HR and payroll operations today.